Top US Banks Value At Risk Soared High: Daily trading risks at top Wall Street banks hit their highest level since 2011 during the first-quarter turmoil, prompting speculation that their capital-intensive markets businesses would be further scaled back.

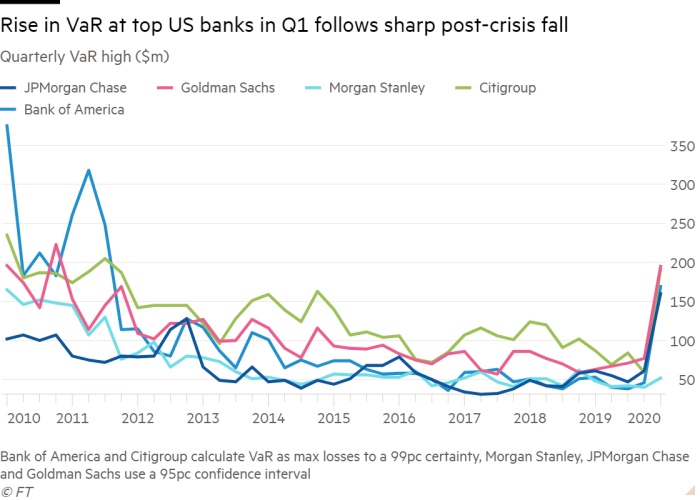

The top five Wall St banks’ aggregate “value at risk”, which measures their potential daily trading losses, soared to its highest level in 34 quarters during the first three months of the year, according to Financial Times analysis of the quarterly VaR high disclosed in banks’ regulatory filings.

The measure is a key input into the total risk attached to banks’ trading businesses, which determines how much capital must be assigned to future trading activities. Spikes in VaR mean trading units need more capital, particularly in the short term, making them more expensive to run.

RELATED: What is Value at Risk – VaR

Devin Ryan, an analyst at JMP Securities, said the first quarter was an “extreme example” of this effect, as record volatility “led to substantially more elevated VaRs than we have seen in some time”.

While markets have been calmer in recent weeks, Mr Ryan added that “if volatility returns and is more lasting, we do think banks could look to further reduce risk, which could drive trading inventories lower”.

Stuart Plesser, analyst at rating agency S&P, said the elevated VaR in the first quarter would be likely to prompt banks to “take another look” at the trading assets they carry on their books. They could use hedges to lower risks, Mr Plesser said, adding: “They may also trim some of the less profitable components of their trading portfolio.”

Banks’ ratio of capital to risk-weighted assets — a key regulatory measure of leverage — fell in the first quarter, putting the allocation of that capital under more scrutiny. Ultimately, the pressure on these groups would “really depend”, Mr Plesser said, on how their underlying profits held up.

A boom in trading revenues was the bright spot in US banks’ first-quarter earnings, at a time when their lending businesses were weighed down by massive provisions for future loan losses.

The absolute levels of VaR are not comparable across banks because they have discretion over the methodology used. But trends can be compared, as banks’ chosen methodologies are consistently applied.

In the first quarter, JPMorgan’s daily VaR touched its highest level since the last quarter of 2009, during the financial crisis. For Goldman Sachs, the peak VaR in the quarter was the bank’s highest since the fourth quarter of 2010, while Citi and Bank of America both recorded their highest levels since the third quarter of 2011.

But Morgan Stanley’s peak daily VaR in the first quarter was only the highest since the fourth quarter of 2018, and less than half its 2010-11 levels. That partly reflects the big cuts the bank made in its trading business half a decade ago.

“We’re very mindful and cognisant of the growth [in market risk] we’ve had,” said a senior trading executive at one of the banks. He added that his bank would have to be “very thoughtful on how much growth we can accommodate”.

The impact of the first-quarter spikes on overall risk will also differ depending on factors such as whether the calculation is based on a longer history or a shorter one. If it is based on a longer history, the first-quarter surge will have a less pronounced impact — if shorter, the opposite is true.

Mr Plesser said the VaR spike would have had a bigger impact on future trading businesses’ capital demands, were it not for the post-crisis introduction of the “stressed VaR” metric. This requires banks to include their worst-ever trading days as part of their ongoing market risk capital calculations.

{kind=link}